{kind=link}

JESSICA MILLER ESSL

Cofounder of M2G Ventures

The last three years when I did the forecast, the area added a hundred stores a year in six major shopping districts.

And looking at the forecast from January of last year, it looked like that was going to be easily surpassable again. However, with COVID hitting, the retail outlook changed significantly, but despite that we actually gained 27 stores, which is more than one would think.

I thought 2020 was going to be the year of optimization, and it was in a major way.

We were going to have some closures, but we were going to forge ahead, that really the closures were going to be related to the fact that we had gained year-over-year a 100 plus stores in major shopping areas that Fort Worth had never seen before and said there was going to be some winners and some losers.

We actually closed 30 food and beverage locations that we know of. And another 30 in major shopping centers, plus 75 national chains.

I was actually shocked by this. There’s not that much data that has come out yet on actual physical counting of closed stores.

Let’s look at national themes we saw in 2020.

National estimates suggests that 20 to 35% of restaurants have closed and will never reopen due to COVID-19. That’s where we currently sit today. There have been 11,000 2020 store closures across the U.S. and 3,400 store openings.

Since 2000, department store sales are down 40%. And then in Holiday 2020, our brick and mortar sales are only down 10% and online is up 44%. This is over Holiday 2019, related mainly to buy online pickup in store with stay at home closures, and with consumer confidence being where people wanted to go pick up in store but buy online.

Why are we not so bad?

In Texas, we added 373,000 people between July 2019 and July 2020. That type of migration is propping up so much. There’s definitely a flight to Texas and specifically DFW. We actually reached our highest home starts in the last decade. COVID, in some ways, you could say has accelerated us for the future.

In Tarrant County, 73 national retailers closed, according to JLL.

In 2019, we had in the high 60s closures as well, and it’s continuing to grow. You could say that COVID exasperated or expedited the ones that were kind of holding on from 2019.

According to Visit Fort Worth, there are approximately 30 food and beverage closures.

From physically counting all the data I received preparing for this presentation, we’re probably at closer to about 70 food and beverage and retail users of note.

If we don’t have the data to support it with sales and landlords aren’t necessarily wanting to shout from the rooftops where their occupancy or at least percentages are, how can you really figure out where we are?

We looked at the data market, using information from JLL.

Retail was actually higher year over year in 2020 for most months and recovered from the previous high in December 2019.

You see food and beverage had a quick initial recovery after April, but it’s now lower than it has been since February 2016. Until we can see all of the COVID mandates go away, it’s going to be really hard for our food and beverage operators in that segment to continue to get out of this.

This is a pretty interesting. The data came from Weizmann, looking at Dallas-Fort Worth, and then our five major retail markets, at least that CoStar reports, Northeast Fort Worth, Northwest Fort Worth, Southeast, Southwest, and Fort Worth CBD.

Our biggest winner is the Alliance sub-market. And our biggest negative change came from downtown, which is not surprising considering the stay-at-home mandates. Our DFW retail market ended better than expected.

If you’re watching the news, you’re going to think you’re going to see numbers in the 70% occupancy range. We still ended 2020 with 91.7%, which is about 2% lower than where we ended 2019 at 93.7%. Even in light of that decline, we have only exceeded the 90% occupant 11 times since 2000 or since the last 31 years. We’re still above that level.

Occupancy dropped as low as 82.1% and never climbed higher than 89.3% in the entire 1990s decades. We’re still above that level for DFW.

Our inventory level reached 200.4 million in retail projects.

Last year when I was reporting, I almost felt like there had to be some shoe to drop, and I thought it would be related to closures from people. Someone coming up with a better concept or thinking through their business plan smarter and getting to the consumer faster. Something was going to have to change.

Prior to this, we were in the longest streak ever of growing occupancy since 2013. In 2020, we’re actually at the eighth consecutive year for 90%. So you can still think that we’re above kind of anemic levels by a large stretch. It still does represent about 4 million square feet of vacated space.

When you look at it in that way, 2020 was a really challenging year. In the last down cycle – 2008 through 2009 – our overall occupancy dropped to 86%. So we’re still 4% above that.

When you take into account that we did not have PPP funding or any of the other kind of additional safety blankets in this last round, I do expect in 2021 we’ll continue to see fallout.

New space deliveries, which is a good thing since we’re going to have to absorb all this additional supply, was the lowest since 2012.

And retail centers are continuing to shrink. An average size for a new retail project in 2020 is 71,000 square feet and it was double that a decade ago. Occupancy rate for Fort Worth is 91.9% compared to 93.3%, so not terrible. Malls across the Metroplex have been our biggest loser dropping to 87.8% occupancy compared to 91% in 2020.

And then in 2018, we’re actually at 87.8%. They’ve basically gone backwards three years.

Twenty years ago, we had 25 enclosed malls. Now we’re down to 13. In Fort Worth, we benefit from mainly having open air shopping centers. I think you’re going to see some higher reported numbers than you would expect.

I’m going to dive into our major areas of retail.

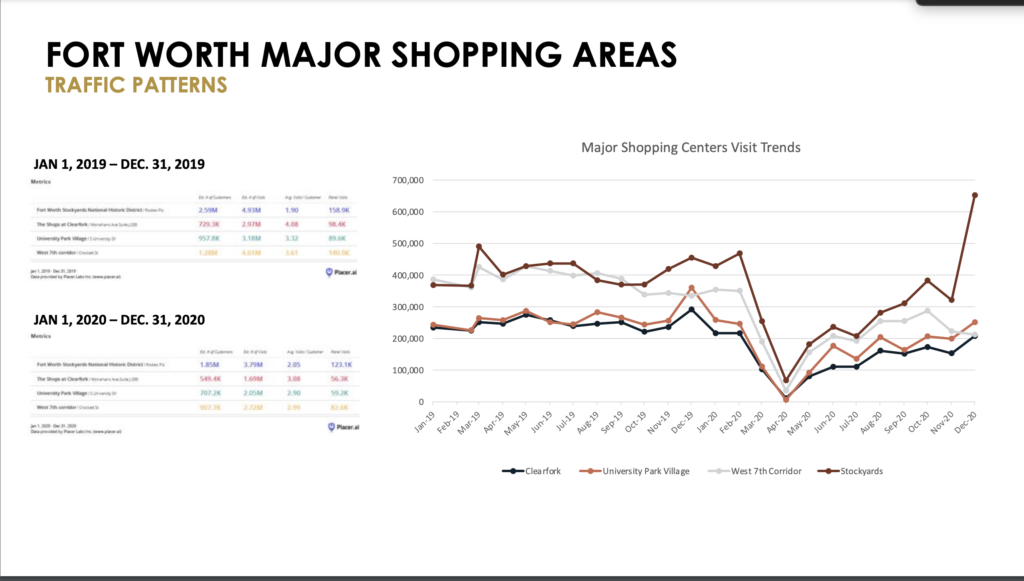

Speaking to things that we can quantify for people versus conjecture, we use Placer.ai to compare the different districts in Fort Worth and you can do this across the country. This is used with cell phone data. It literally tracks you where you go. It’s pretty creepy, but it’s very accurate.

We compared the foremost major retail districts from Jan. 1, 2019, to Dec. 31, 2020. Those four are, Clear Fork, University Park Village, West 7th Corridor, and the Stockyards.

They’ve all followed the same trendline for the most part in terms of that big dip is in April of 2020, which is obviously right after retail sales dropped off the face of the Earth. And they have been steadily climbing. The interesting thing is customer frequency is increasing in some districts.

In the Stockyards, its mainly related to new development. People are excited about all the new shops opening. And in addition to that, because regional travel has become an even bigger thing with the airline business down, places you can get to by car and still have that staycation or vacation are going to go up. We can see that evidenced by the Stockyards’ continued growth. CBD, ClearFork and Stockyards are all starting to show signs of recovery. The Stockyards is actually higher than it’s ever reported highest number in the last two years.

Looking at traffic patterns, what you should take away is lunch traffic has significantly declined across all major shopping areas, creating more of a separation between why somebody would go to a shopping center, for example. Before, some of our major areas really benefited from a large office population. Today, that’s not necessarily as much the case or people are staying more in their office and having lunch there or eating at home.

In some places, average stay has gone up. Again, if people are going to get out and shop and do things, they’re going to want to stay at a place that has more to do than just shop, eat, things of that nature. The Stockyards has gone up. The others have stayed either flat or slightly down.

I’m going to dive into each one of the major shopping centers.

A lot of landlords don’t even really know where they’re at because they’re depending on retailers to stay open and they could close at any point.

What’s going to happen in 2021?

We’ve got some exciting announcements, but for the most part, people are really trying to make it and hunker down and get excited for this to be over.

The Shops at Clear Fork only had three closures, which is really good.

Waterside looks very stable, very full.

WestBend did have some turnover, but has done a really good job. And you’ll see this in 2021, re-tenanting the mix and different retailers that are going to be even better for the project. So overall it’s going to come out better post COVID.

We’ve been reporting this for the last two years, but WestBend is going to be adding a second phase.

West 7th and Crockett Row performance was not surprising because of the stay-at-home orders. We do expect this to stabilize somewhere in Q3, Q4 when people start to feel more comfortable about coming back out.

The Foundry District had six openings in 2020, two closures in 2020, and we’ll have another opening in 2021. It’s 90% leased. This is from personal knowledge on property with tenants using their space for multiple different reasons. It’s kind of a flex project between some retail, some office, and then some industrial.

In 2021, you’re going to see the White Settlement Bridge open for the first time in five years, which is really going to add a lot of much needed just East-West thoroughfare through the central part of Fort Worth.

We survived, and with a very low number of closures. Closures experienced were from businesses that were likely struggling before the pandemic.

We’re seeing a surge in arts investment through murals, commissions, and partnerships with artists. This is no doubt related to pioneering work to include art in the M2G projects and our recent Cultural District designation.

It’s a big deal to get the Cultural District Designation from the Texas Commission on the Arts, making the Near Southside one of only 42 cultural districts in the state of Texas.

There was strong small business support from the community during the pandemic. We are seeing many new businesses come to the table for lease inquiries, especially food oriented businesses, despite the pandemic, because this district has done a great job of keeping the community as customers.

Last but not least, what do I think is going to happen in 2021?

I think there’s going to be a year of recovery with more closures. I think PPP is going to dry out for a lot of people, and then their profits or savings will dry out, so we’re going to see more closures.

We’ll see a slight increase in occupancy. There’s going to be more focus on mixed use and adaptation of existing retail and shoppers are going to start feeling safe in Q3 and Q4. We’ll start to rebuild our food and beverage program, and I’m going to make a bold prediction that Fort Worth is going to move from the 13th largest city to the 12th largest, and I hope it’s the 11th.

And I think the rest of the United States is going to take notes.

This is a presentation made at the Real Estate Forecast 2021 from the Greater Fort Worth Real Estate Council.

By the numbers:

The Shops at Clearfork

2020 Closures – 3, 2021 Openings – to be determined.

Waterside

Sur La Table and Taco Diner (closed Sept 2019) both closed with Taco Diner eventually closing both Fort Worth locations. Taco Diner is being replaced by The Rim.

WestBend

Snapshot: 90% leased total project, $500 sales per square foot

2020 Closures – 4; 2021 Openings – 4 plus.

New Johnnie O (first brick and mortar in the country) opening Feb. 5 in former Pax and Parker space.

Momaka Bowl opening in the Marine Layer space. Cool concept in Waco and Fayetteville.

Market by Macy’s is now open and the store looks good. Some elevated brands but this will change soon.

Leases are out on Bartaco space. More to come on who but we can’t say right now.

Zapp Kitchen is opening in a couple of weeks in the Popbar space. Great Thai from Dallas.

Ascension Coffee is killing it.

We are VERY close in getting the space between Dear Hannah and Suzie Cakes leased as well.

WestBend Phase II – Future 2023 plus

– 328 multifamily units

– 25,000 square feet of retail and restaurant

– 142 room boutique hotel

West 7th and Crockett Row

2020 executed leases – 2

2020 closures – 8; 2021 openings – to be determined

Once workers get back in the office completely, Q3 and Q4, they expect this to start stabilizing.

Foundry District

– 2020 – 97% leased

– 2020 openings – 6; 2020 closures – 2; 2021 openings – 1

– 2021 – 98% leased

– District benefited from multiple tenants using their space for multiple reasons including fulfillment and production

– Blackland will expand, complete improvements to the overall physical landscape of the area, and the White Settlement Bridge will open after five plus years of being under construction

Near Southside

2020/2021 signings and openings – 37

– PS1200 is breaking ground at 1200 6th Ave.

– 701 W. Magnolia significant expansion with pedestrian mall

– Nobleman Hotel

– Expansion of Hotel Revel

– 305 W. Daggett retail by Bohannon breaking ground

– District overall expansion

Stockyards Mule Alley

$200M investment including:

– 180,000 square foot reinvention of the horse and mule barns

– 93% leased or at lease

– 3 stores opened in 2020; seven more in 2021

– No closures

Cowtown Coliseum

– Another 40,000 square feet plus will open this year

– Marriott Collection Autograph Hotel Drover Grand Opening March 2021, along with Lucchese collection

– Future phase to come

– Sales are off the charts across all price points

– Coliseum is now being operated under Stockyards Heritage Ownership